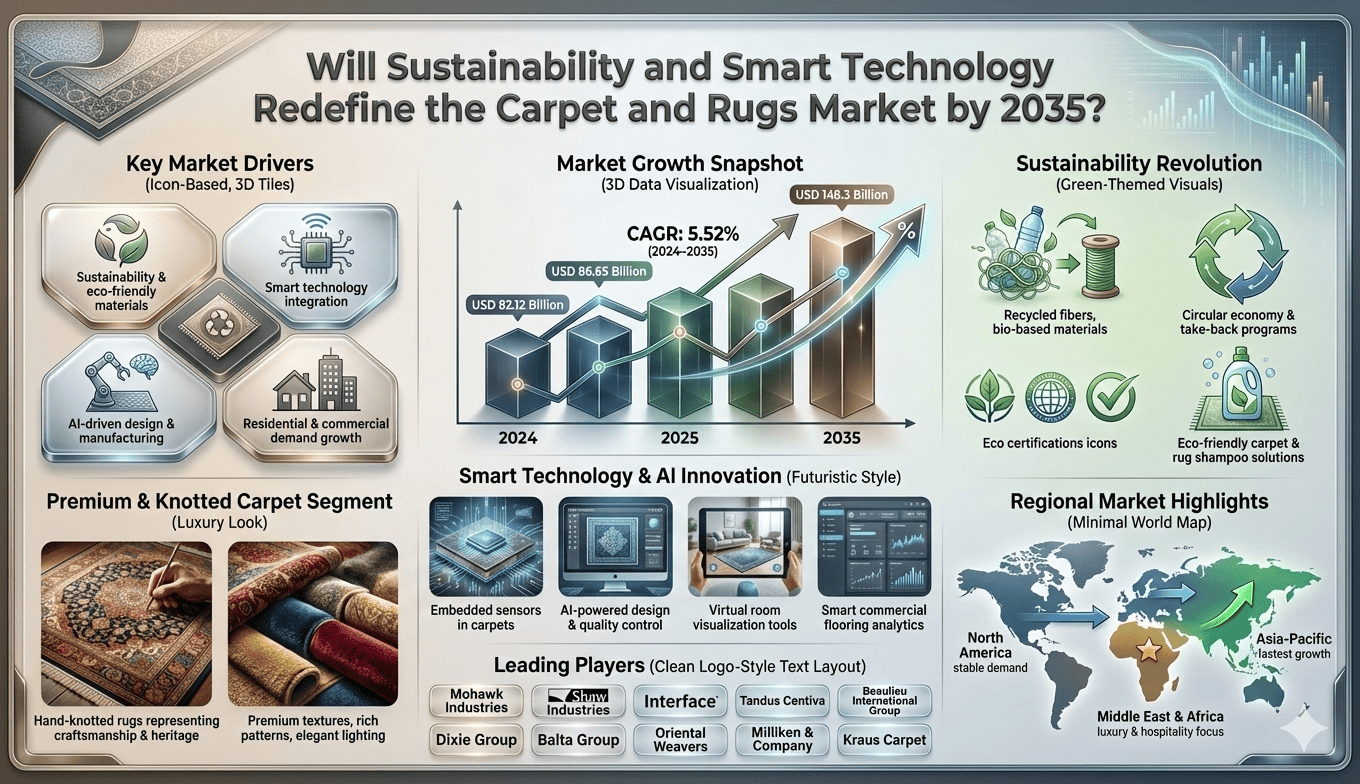

The global carpet and rugs market is experiencing steady growth despite mounting geopolitical pressures across key manufacturing and trade corridors. The market was valued at USD 82.12 billion in 2024 and is projected to reach USD 86.65 billion by 2025, expanding at a compound annual growth rate (CAGR) of 5.52% from 2025 to 2035. By the end of the forecast period in 2035, the market is expected to attain a valuation of USD 148.3 billion. This growth trajectory is driven by rising demand for sustainable flooring solutions, increasing renovation activities in residential and commercial sectors, and the integration of smart technology into textile products. However, escalating tensions in critical shipping routes and supply chain vulnerabilities pose significant risks to the market’s stability and cost structure.

Key Market Players and Competitive Landscape

The carpet and rugs market is characterized by intense competition among established industry leaders and emerging regional players. Major companies profiled in the market include Mohawk Industries (US), Shaw Industries (US), Interface (US), Tandus Centiva (US), Beaulieu International Group (Belgium), Dixie Group (US), Balta Group (Belgium), Oriental Weavers (Egypt), Milliken & Company (US), and Kraus Carpet (Canada). These companies are investing heavily in sustainable manufacturing processes, eco-friendly materials, and digital innovation to maintain their competitive edge. Strategic partnerships, mergers and acquisitions, and geographic expansion are key strategies being employed to capture market share in emerging economies where urbanization and infrastructure development are accelerating.

Regional Analysis and Market Dynamics

North America currently holds a significant share of the global carpet and rugs market, driven by robust demand from the residential renovation sector and stringent environmental regulations that favor sustainable products. The United States remains the largest contributor to regional revenue, supported by a well-established distribution network and strong consumer preference for premium quality flooring. Europe follows closely, with countries like Germany, France, and the United Kingdom demonstrating consistent demand for luxury carpets and innovative designs. The Asia-Pacific (APAC) region is projected to witness the fastest growth during the forecast period, fueled by rapid urbanization, rising disposable incomes, and expanding construction activities in China, India, and Southeast Asian nations. South America and the Middle East & Africa (MEA) are emerging markets with untapped potential, although infrastructural challenges and economic volatility may temper growth rates.

Access Free Sample Copy – https://www.marketresearchfuture.com/sample_request/4154

Market Segmentation and Product Categories

The carpet and rugs market is segmented based on product type, material composition, end-user application, and geographic region. By product type, the market encompasses tufted carpets, woven carpets, needle-punched carpets, and knotted rugs, with tufted carpets commanding the largest market share due to their cost-effectiveness and versatility. Material-wise, synthetic fibers such as nylon, polyester, and polypropylene dominate the market, although natural fibers like wool, jute, and silk are gaining traction among environmentally conscious consumers. End-user segmentation includes residential, commercial (offices, hotels, retail spaces), and industrial applications, with the residential sector accounting for the majority of demand. Within residential applications, living rooms and bedrooms are the primary areas driving carpet and rug purchases, while commercial establishments prioritize durability and aesthetic appeal.

Growth Drivers and Market Trends

Several factors are propelling the growth of the carpet and rugs market in the coming decade. The shift in consumer preferences toward sustainable and eco-friendly materials is a primary driver, as manufacturers increasingly adopt recycled fibers, biodegradable backing materials, and low-emission production processes to meet regulatory standards and consumer expectations. The integration of smart technology, including stain-resistant coatings, antimicrobial treatments, and modular designs that facilitate easy replacement and maintenance, is also enhancing product appeal. Rising renovation activities in aging housing stock, particularly in North America and Europe, are creating sustained demand for replacement carpets and decorative rugs. Additionally, the hospitality and corporate sectors are investing in premium flooring solutions to enhance interior aesthetics and improve occupant comfort.

Emerging trends include the growing popularity of customized and designer rugs, driven by millennial and Gen Z consumers seeking personalized home décor. E-commerce platforms have democratized access to a wider variety of products, enabling consumers to compare prices, view virtual room renderings, and access niche designs that were previously available only through specialty retailers. Furthermore, the circular economy model is gaining momentum, with companies offering take-back programs and recycling initiatives to reduce textile waste. These trends collectively indicate a market that is not only expanding in value but also evolving in response to changing societal values and technological advancements.

Geopolitical Tensions and Supply Chain Vulnerabilities

The escalating conflict involving Iran, Israel, and the United States is creating unprecedented disruptions across the carpet and rugs market, particularly affecting raw material sourcing, manufacturing logistics, and export-import dynamics. Iran has historically been a significant producer of hand-knotted Persian rugs, renowned for their craftsmanship and cultural heritage. Sanctions, trade restrictions, and political instability in the region have severely constrained the availability of these premium products in international markets, forcing retailers to seek alternative suppliers or face inventory shortages. Additionally, the broader Middle Eastern conflict is impacting the supply of petrochemical derivatives used in synthetic carpet fibers, as production facilities in affected regions face operational challenges and insurance costs skyrocket. Shipping routes through the Strait of Hormuz and the Red Sea—critical arteries for energy and chemical transport—are under heightened security threats, leading to delays, rerouting, and increased freight costs that ultimately trickle down to consumers.

Access Full Report – https://www.marketresearchfuture.com/reports/carpet-and-rugs-market-4154

GLOBAL SUPPLY CHAIN & MARKET DISRUPTION ALERT

Escalating geopolitical tensions in the Middle East, particularly around the Strait of Hormuz and the Red Sea, are creating significant disruptions across global energy, chemicals, and logistics markets. Critical shipping corridors are under pressure, with major oil, LNG, petrochemical, and raw material flows at risk, triggering supply chain delays, freight cost surges, insurance withdrawals, and heightened price volatility. These disruptions are increasing operational risks and cost uncertainties for industries dependent on global trade routes and energy-linked feedstocks.

Frequently Asked Questions (FAQs)

Q1: What are the key differences between synthetic and natural fiber carpets in terms of durability and maintenance?

A: Synthetic fiber carpets, particularly those made from nylon and polyester, offer superior stain resistance, moisture repellency, and color retention compared to natural fibers. They are generally easier to clean and maintain, making them ideal for high-traffic commercial spaces and households with pets or children. Natural fiber carpets, such as wool and silk, provide exceptional softness, thermal insulation, and aesthetic appeal but require more delicate cleaning methods and are susceptible to moisture damage. Wool carpets, while more expensive, are naturally flame-resistant and biodegradable, aligning with sustainability goals. The choice between synthetic and natural fibers depends on budget, usage patterns, and environmental considerations.

Q2: How is the carpet and rugs industry addressing environmental concerns and moving toward circular economy practices?

A: The industry is implementing several initiatives to reduce its environmental footprint, including the use of recycled PET bottles and reclaimed fishing nets in carpet production, adoption of closed-loop manufacturing systems that recycle production waste, and development of modular carpet tiles that can be selectively replaced rather than discarding entire installations. Leading manufacturers are also investing in chemical recycling technologies that break down old carpets into their base polymers for reuse. Take-back programs allow consumers to return old carpets for recycling, diverting millions of pounds of textile waste from landfills annually. Additionally, certifications such as Cradle to Cradle and Green Label Plus are helping consumers identify products that meet stringent environmental and health standards.

Read Our Related Report:

Carpet Extractor Market –

https://www.marketresearchfuture.com/reports/carpet-extractor-market-36494

Home Bedding Market –

https://www.marketresearchfuture.com/reports/home-bedding-market-8790

Home Decor Market –

https://www.marketresearchfuture.com/reports/home-decor-market-11525

Textile Home Decor Market –

https://www.marketresearchfuture.com/reports/textile-home-decor-market-24239

Home Care Service Market –

https://www.marketresearchfuture.com/reports/home-care-service-market-33384